Warning: Undefined variable $class in /home/netst/kuno-cpa.co.jp/public_html/incorporation-in-japan/wp-content/themes/tokyo_c_establishJ/header.php on line 74

class="wp-singular page-template-default page page-id-71 wp-theme-tokyo_c_establishJ ma gecko">

Tokyo Consulthing Firm

M&A

【M&A in Japan】

Mergers and Acquisitions (M&A) refers to the process of one business purchasing another business and blending the two together. Merging and acquiring a business is also known as a “take over”. Mergers and acquisitions and corporate restructuring represent an important aspect of the corporate finance world.

VEvery day, specialized firms and investment bankers around the world arrange M&A transactions, which bring separate companies together to form larger ones. When they’re not creating big companies from smaller ones, corporate finance deals do the reverse and break up companies through spin-offs, carve-outs or tracking stocks. Deals can be worth hundreds of millions, or even at times billions of dollars. They can dictate the fortunes of the companies involved for years to come. For a CEO, leading an M&A operation can represent the highlight of a whole career.

On the other hand, there are certain challenges faced by M&A operators. For instance, in certain countries, regulations prohibit the purchase of land or any type of property or business, making it impossible for M&A to develop. Within Asia, there has also been a surge in the merging of businesses with one another, and in some cases, hostile take-overs. Finally, mergers and acquisitions trends are cyclical, and with banks and other lending institutions refusing to extend credit or make loans, the merging of businesses can slow down dramatically.

【Process】

Going through an M&Aamp; deal can be an intimidating process (for both the mergers and acquisitions teams), but thankfully, this process follows consistent steps. Here’s the step-by-step process that nearly every M&A deal follows:

1.Compile a target list

A list of suitable sellers or buyers is a must-have for a transaction to take place.

2.Contact the targets

Making a phone call and discussing the target’s interest is important. Such discussions allow prospectors to gauge the target’s interest level, and whether proceeding makes sense. Knowing how to make a pitch is an art, and being a buyer is actually far more difficult than being a seller.

3.Send/receive a teaser

The teaser (sometimes called an executive summary) is the document the seller sends the buyer to give him or her just enough information (product, customers, problem the company addresses, and some high-level financial details) to make the buyer want to learn more. The teaser is usually anonymous; that is, the buyer doesn’t know which specific company is sending the document.

4.Sign a confidentiality agreement

Both sides agree to keep discussions and materials related to the deal confidential.

5.Send/review the Confidential Information Memorandum (CIM)

The CIM (or deal book) is the seller’s bible, as it provides all the information (including company history, product descriptions, financial characteristics, etc.) the buyer needs in order to determine whether it is possible for him or her to make an offer.

6.Submit/solicit an Indication of Interest (IOI)

The buyer expresses interest in entering a deal by submitting this simple written offer, most often with a valuation range rather than a specific price.

7.Conduct management meetings

Buyer and Seller get a chance to meet face to face. Through these meetings, the provides the potential buyer with updates related to the business, as well as guidance for future performance. Additionally, both sides gauge their mutual compatibility.

8.Ask for or submit a Letter of Intent (LOI)

Based on the material in the CIM and on the updates from the management meetings, the buyer submits this detailed offer with a firm price.

9.Conduct due diligence

In the due diligence phase, the buyer closely examines the seller’s books and records to confirm everything claimed by the seller.

10.Write the purchase agreement

Both parties materialize the deal in a legally binding contract.Close the deal

11.Close the deal

A list of suitable sellers or buyers is a must-have for a transaction to take place.

12.Handle any post-closing adjustments and integration

Closing isn’t the end of the deal. Both the buyer and seller usually have some post-closing financial adjustments, and the buyer has to integrate the acquired company into the parent company or make sure it can continue to operate as a standalone business.

【Due Diligence】

Mergers and Acquisitions (M&A) transactions are among the most complex activities a business can undertake. In today’s global market, where not all information is transparent, these transactions present an even greater challenge. Companies include a substantial part of their value creation/synergy targets in the acquisition purchase price…

Due to expected future defaults and economic issues, management – more than ever before – wants to quantify the risk of not being able to meet those targets. Thus, due diligence is a crucial aspect of any M&A deal, as it is the main process that allows to evaluate the health levels of the parties involved, and therefore, of the entire deal. Tokyo Consulting Group consultants help organizations evaluate the financial, commercial, regulatory and other situations of potential merger candidates and understand the opportunities and challenges that may arise from a M&A operation.

Our M&A Japan team includes auditors, former regulators, forensic accountants and experts who provide investigative analysis of businesses including background history, results/projections, cash flows, market analysis, management information, commercial and operational issues, and systems and controls. Our Due Diligence services help companies to:

・Make sure potential issues are addressed early on in the process

・Identify potential management or cultural challenges

・Develop, evaluate and validate quantitative financial models that support critical decisions

・Ensure awareness of regulatory and other compliance issues

・Document the target company’s business processes and control points

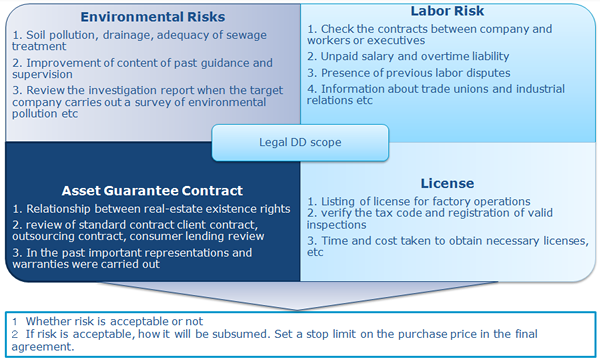

Legal Due diligence

Legal due diligence consists of an examination of the legal affairs of the target company in order to uncover any risks, and to provide detailed information regarding the company’s legal situation. A legal due diligence exercise often improves the bargaining power of the buyer. The objectives of legal due diligence vary from case to case, but some of the typical objectives are summarized below:

・Gathering of information about the target company

・Uncovering the target company’s strengths and weaknesses, risks and advantages in connection with the transaction

・Minimizing the risk of unexpected situations

・Improvement of the seller’s bargaining position

・Identification of areas where representations and warranties from the seller should be obtained in the acquisition agreement.

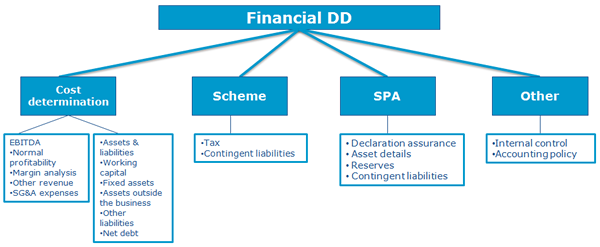

【Financial Due Diligence】

Financial Due Diligence refers to the process of investigation into the financial affairs of the target company that has a material impact on the prospects of the business. A Financial Due Diligence review may not only look at the historical financial performance of a business, but can also consider the future financial performance.

The initial stage of the Financial Due Diligence process determines the ability of the company to bring a profit and the probability of the success of the project. Within the financial review, Tax Due Diligence is also carried out. The purpose of this is to investigate the possibility of any tax burden, and if possible, effectively and legally exclude it.

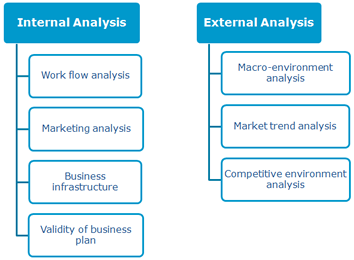

【Business Due Diligence】

The business due diligence process includes the gathering, analysis and interpretation of financial, commercial, legal and marketing information. It is divided into two components – external and internal. The purpose of this process is to assess the shape and health of the business with regard to external factors (competitors), in order to rightly assess the potential of an M&A deal.